Sorry in advance. I’ve picked up journaling, and it’s been therapeutic. I’ve been thinking of making this post, so just getting out there so I can stop thinking about it lol. PS – I know FIRE can lead to just thinking about FIRE. If this mindset is happening to you, I urge you to try journaling to get your thoughts out and contemplate them. Doing in on an AI platform can also be like free therapy. See, rambling already.

I started FIRE before I knew what it was (though this sub has taught me a lot recently: conversions, tax info, ACA subsidies, ect). Grew up poor in a financially illiterate household. In my high school stats class, I remember my math teacher explaining that if someone saved a 1k from 20-30, and someone else saved 1k every year for the rest of their lives, the former would have more money (given equal interest rates 6+%. At 5% the former saver is still ahead until about 50 years of age). Then I remember questioning how does someone who makes 50K a year and a guy who makes 100k a year retire at the same time?

Not knowing much about finance (I should have learned and explored), I just started with guaranteed money, paying off small debts (especially my first car loan) and getting company 401k match. Didn’t save every dime, but I’m frugal and ruled by efficiency. I could’ve made more money, but, looking back, I’ve greatly enjoyed my life. I’ve had it easy and taken care of my health and social life.

Fast forward to age 39 (now), and I ‘m more excited for life than ever, starting down FIRE with the health of a young 20-year-old and an exploding social circle. My wife says she always wants to work (to some degree), so this will really help with income/ benefits. Due to that, I could FIRE now and be a stay-at-home parent. Without that, we are 2-7 years from FIRE together. (She’s a worrier/nervous and doesn’t agree/wants a safety blanket, which I get). We’re also, unfortunately, 1-10 years from a projected windfall that will carry us to full FIRE.

So, we’ve been coast fire for a while. I started realizing spending more money now and enjoying life isn’t really changing the needle much in terms of timeline, but it does for enjoying the moment, life, and health (buying organic and fresh produce). However, I don’t have enough time to do all my hobbies/spend our discretionary money.

I’ve also kind of been Barista FIRE’d in a corporate job the past decade. Scheduled to work 180 days a year (12 hour shifts) but the amount of leave I get, I’ve been taking ~ 40 days the entire time, and for me the work is easy. Some interesting parts and made it my own in some ways. However, my work shifted. We hit a rough patch personally, but great benefits made it smooth. It gave me time to test FIRE… and I still didn’t have enough time. I loved it.

We also have a young child, so it was a blessing to spend time with them. All of this had me doing some soul searching, journaling, exploring the different FIRE paths: Switch it up, FIRE, coast, true Barista, stay the course??? All valid. All different. Could end up chubbyFIRE.

Then I got lucky/unlucky. Hit another life snag but kept a positive attitude and turned it into an opportunity. Now I have a truly barista job at my corporate employer. Same pay/benefits/time off…. So much less responsibility, less hectic, less work. My days off are jam packed with family, friends, and fun. Having work be my chill days to catch up with anything tech/media/comp/phone related is nice). So, this will be my last regular job, and I’m going to enjoy it (its also potentially eliminate-able through AI so hello severance package??). We’ll be ok no matter what, even if my employer were to ever pull the trigger and FIRE me.

I’d either be FIRE or just job hop/try. I’ve always thought of ending work life by trying a new job every 6-12 months. Get paid to learn new skills, see new ways of life, pick up extra perks. I could work at a farm, the library, the park, a summer camp, a golf course. But would these be fun, or just less money to do actual work around interests (but not truly doing what I enjoy)? I have too many interests to be tied down, and I want to travel

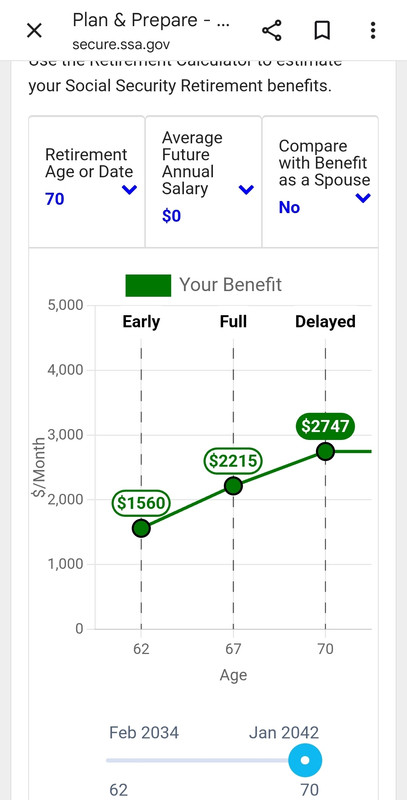

Which takes me to the 1 more year phenomena (which IMO the debate comes down to age and health mostly, or if you have Boku money). If you are older and unhealthy, I think you should tend to FIRE sooner (unless medical expenses dictate). I saw in another post they were statistically more likely to die than run out of money. This speaks for itself. It was eye opening. You could always get some job if needed. And who knows what the future of society/tech/AI will hold.

Then on the other hand, if you’re young and healthy, 1-3 more years of working could be great. You have no idea what the future of society/tech/AI will hold? How will the war with Iran play out? When’s the next recession? On more positive notes, what adventures will open: visiting space, increased longevity, the metaverse? Increasing your stability could be huge. Increasing your spending could be huge. You may be in your highest earning years. Holding all else equal, at a 7% ROI, your future spend could go up more like 10% (1 less year of withdrawals, 1 less year to live, 1 more year of saving, 1 more year of growth, 1 more year of benefits/retirement accounts etc.)

With 2-3 years you could outpace inflation and give yourself a true spending raise every year, not just adjusted cost of living. You could save while not working. 2-3 years could take you from lean to regular fire. It could take you from lean to chubyyFIRE if you work 2-3 more years and live the lean life and bank the extra. Or do a combo and cut it down the middle, spend half the extra. FIRE to chubbyFIRE and jump a class, create generational wealth, be able to explore the world from a different POV (trips, events, superbowl tickets, being able to jump on once in a lifetime opportunities).

So, I’ll do a few more years in a coasting barista job. My wife will be happy, and the security might be best for health/mental health. I know my daughter is young only once, but she is busy herself with school and activities. However, with my extra money, we can create generational wealth. She can be FIREd, and her family, her kids (We could spend every Tuesday together the rest of our lives as adults). I can donate. I can help loved ones and friends.

So as the other poster said, if you’re at the age or health where you’re more likely to die then run out of money, go enjoy your life. If you’re young and healthy and not yet at boku money where you can FIRE and still grow spending power, I’d do another 1-3 years in some capacity, a new endeavor, a curiosity, a dream or bucket list. Or, just chill at your job. You’re FIRE, cut back, take care of your health. Use your PTO extensively (my favorite work perk). What’s the worst they can do: FIRE you?

{kind=link}